Build a Three-Fund ETF Portfolio for Retirement

- Expense ratios near 0.03% to 0.10% changed the retirement portfolio math.

- A diversified investor no longer needs 12 funds, manager overlap, or a rotating list of sector bets to get global market exposure.

- Three broad ETFs can cover the core: U.S.

The question is not whether a three-fund ETF portfolio is clever. It is whether the allocation is correctly sized for the investor’s retirement horizon, volatility tolerance, and withdrawal plan. That is the practical answer behind how to check build a three-fund ETF portfolio for retirement: start with the asset classes, not the tickers.

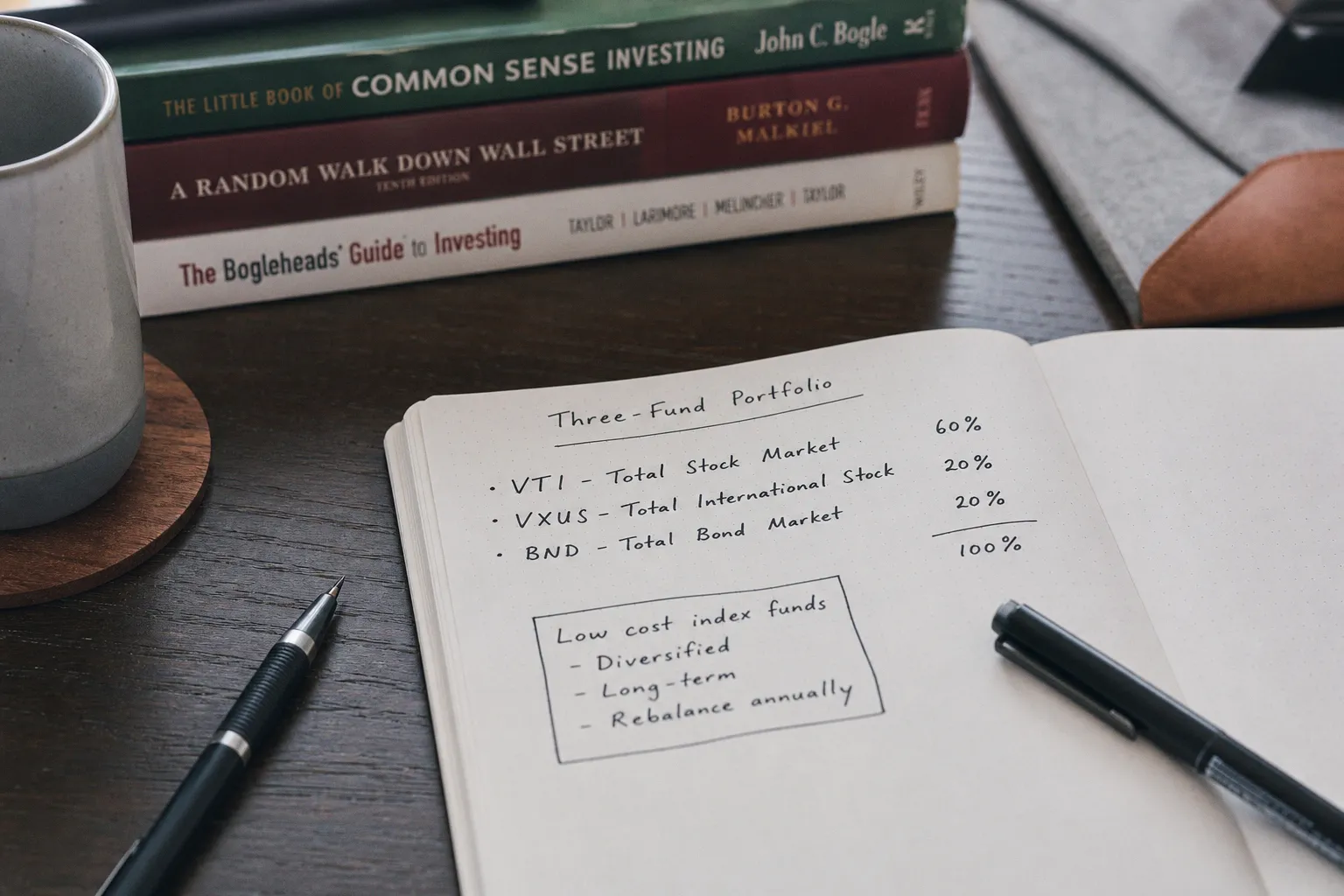

The architecture: three funds, three jobs

A classic three-fund portfolio uses one ETF for each major allocation sleeve:

1. Total U.S. stock market

2. Total international stock market

3. Total bond market

That structure is not minimalism for its own sake. It is a risk-control framework. Each fund has a separate function.

The U.S. equity ETF captures domestic public companies across market capitalizations. The international ETF adds non-U.S. developed and emerging markets exposure. The bond ETF reduces portfolio volatility and provides an income-producing sleeve that can be rebalanced into stocks after drawdowns.

The mechanics are clean:

| Portfolio sleeve | Core function | Typical ETF example | Main risk |

|---|---|---|---|

| Total U.S. stock market | Long-term equity growth | VTI | Equity market drawdowns |

| Total international stock market | Global diversification | VXUS | Currency, regional, and geopolitical risk |

| Total bond market | Volatility control and income | BND | Interest-rate and credit risk |

VTI, VXUS, and BND are common Vanguard examples, not the only valid implementation. The same structure can be built with comparable low-cost ETFs from other issuers if they track broad indexes and avoid narrow factor tilts.

The point: the portfolio owns markets, not forecasts.

A three-fund portfolio is not designed to beat the market. It is designed to stop the investor from needing to guess which market wins next.

That distinction matters. A concentrated portfolio can outperform. It can also fail for reasons that have nothing to do with retirement needs. A three-fund strategy accepts market returns and focuses on the variables the investor can actually control: fees, allocation, taxes, contribution discipline, and rebalancing.

The ETF screen: low cost first, then coverage

The ETF selection process should be mechanical. Do not begin with recent performance rankings. Those rankings mostly show what has already happened. Begin with exposure and cost.

Broad-market ETFs used in this strategy usually carry expense ratios around 0.03% to 0.10%. That fee range is low enough that cost drag becomes small, but it still compounds. A 0.70% annual fee on a retirement portfolio is not a rounding error over 25 or 30 years.

The screen should focus on five variables:

- Index breadth. The U.S. stock sleeve should hold thousands of companies across large-, mid-, and small-cap segments. A large-cap-only ETF can work in a different strategy, but it is not the same as total market exposure.

- International completeness. A proper international ETF should not stop at Europe and Japan. Emerging markets exposure is usually part of total international coverage.

- Bond quality and duration. A total bond market ETF typically includes government and investment-grade corporate bonds. Duration matters because longer-duration bonds are more sensitive to rate moves.

- Expense ratio. The target range for broad index ETFs is commonly near 0.03% to 0.10%. Higher fees need a clear structural reason.

- Trading liquidity. Large, heavily traded ETFs usually have tighter bid-ask spreads. This reduces implementation cost, especially for larger orders.

A clean implementation might look like this:

| Role | ETF type | Example | What it should avoid |

|---|---|---|---|

| U.S. equity | Total U.S. stock market ETF | VTI | Sector concentration or active stock picking |

| International equity | Total ex-U.S. stock market ETF | VXUS | Developed-only exposure if emerging markets are intended |

| Bonds | Total U.S. bond market ETF | BND | Excessive credit risk or long-duration concentration |

The ETF ticker is less important than the job being performed. A portfolio with three funds can still be poorly built if the funds overlap heavily or tilt into the same risk factor. A U.S. total market ETF plus a large-cap growth ETF plus a technology ETF is not a three-fund retirement strategy. It is one equity bet in three wrappers.

Why the bond fund is not optional by default

In bull markets, the bond sleeve looks inefficient. It usually trails equities. That is the cost of risk control.

Bonds exist to lower drawdown severity, supply rebalancing capital, and reduce sequence-of-returns risk near retirement. Sequence risk is the damage caused when withdrawals begin during a market decline. A portfolio that must sell equities after a sharp drawdown can lock in losses and reduce future compounding capacity.

A younger investor with a long horizon may hold only a modest bond allocation. Some may choose 80% to 90% stocks. That is still an allocation decision, not a reason to ignore fixed income permanently.

The old rule of thumb, “100 minus age” for bond allocation, is often considered conservative for modern investors with longer life spans and extended retirement periods. It remains useful as a reference point, not a command.

Asset allocation: the portfolio’s real engine

The three funds are the parts. Asset allocation is the machine.

A 90/10 stock-bond portfolio and a 60/40 stock-bond portfolio can use the same ETFs and behave very differently. The first has higher expected volatility and larger drawdowns. The second trades some growth potential for stability.

The most common decision points are:

1. Stock versus bond allocation. This controls the portfolio’s broad risk level.

2. U.S. versus international stock allocation. This controls geographic exposure.

3. Rebalancing rules. This controls whether the portfolio stays aligned with its target.

There is no single ideal U.S.-international split. Investors often debate structures such as 60/40 or 70/30 within the equity sleeve. The right answer depends on home-country preference, currency exposure, and confidence in global diversification. What should be avoided is pretending the split is scientifically exact.

A sample allocation framework:

| Investor profile | Stocks | Bonds | U.S. stock share of equity sleeve | International share of equity sleeve |

|---|---|---|---|---|

| Long horizon, high volatility tolerance | 90% | 10% | 60%–70% | 30%–40% |

| Mid-career, moderate volatility tolerance | 80% | 20% | 60%–70% | 30%–40% |

| Approaching retirement | 60%–70% | 30%–40% | 60%–70% | 30%–40% |

| In retirement, withdrawal-focused | Varies | Varies | Varies | Varies |

These are not personalized recommendations. They show how the structure changes when the objective changes.

The retirement horizon sets the first constraint. A 32-year-old investor with stable income and no near-term withdrawal need can usually absorb more equity volatility than a 62-year-old preparing for portfolio withdrawals. The same bear market has different consequences for each.

Risk tolerance sets the second constraint. Many investors overestimate it during rising markets. The test is not whether a 90% stock allocation looks efficient in a spreadsheet. The test is whether the investor can hold it through a 30% equity drawdown without abandoning the plan.

Cash-flow stability sets the third constraint. A household with irregular income may need a larger cash reserve outside the portfolio. The three-fund ETF portfolio should not be forced to cover short-term spending shocks.

Rebalancing: the control system

Rebalancing is the part of the strategy that looks simple and behaves hard.

When stocks rise faster than bonds, the portfolio becomes more aggressive. When stocks fall sharply, the portfolio becomes more conservative unless new money or bond sales are used to restore the target. Rebalancing counters that drift.

A common trigger is a 5 percentage point deviation from the target allocation. Annual rebalancing is also common. Some investors use both: check once or twice a year, but trade only when drift is large enough to matter.

Example: target allocation is 80% stocks and 20% bonds.

If a rally moves the portfolio to 86% stocks and 14% bonds, the equity sleeve has drifted 6 percentage points above target. A rebalance would sell some stocks or direct new contributions into bonds.

If a downturn moves the portfolio to 74% stocks and 26% bonds, the portfolio has become more conservative. A rebalance would buy stocks using bond proceeds or new contributions.

Rebalancing is not market timing. It is the enforcement mechanism for the risk level already chosen.

The distinction is critical. Market timing asks, “What will happen next?” Rebalancing asks, “What did I agree to own?”

A practical rebalancing hierarchy:

1. Use new contributions first. Direct incoming cash toward the underweight ETF. This reduces selling and may improve tax efficiency.

2. Rebalance inside tax-advantaged accounts when possible. Retirement accounts can make reallocations cleaner than taxable accounts, where realized gains may create tax consequences.

3. Use a drift band. A 5% threshold avoids excessive trading while still keeping the portfolio close to target.

4. Do not rebalance on headlines. Rate moves, election cycles, oil shocks, and earnings scares are not allocation rules.

5. Document the target allocation. A written target reduces ad hoc changes during volatility.

For investors tracking household costs alongside portfolio risk, energy and utility prices can affect monthly cash flow and contribution capacity; industry coverage such as energy and utility market updates can be useful context without becoming an investment signal.

That last clause matters. Macro information can explain pressure on budgets. It should not turn a three-fund portfolio into a commodity-timing vehicle.

Market volatility: what the three-fund structure does and does not solve

A three-fund ETF portfolio remains exposed to market risk. It can lose money. Global equities can fall together. Bonds can decline when interest rates rise. International diversification can lag U.S. stocks for long periods.

The structure reduces idiosyncratic risk. It does not eliminate systemic risk.

Idiosyncratic risk is company-specific or sector-specific risk: a failed product cycle, a regulatory hit, a bank balance-sheet problem, a single-country shock. Broad index funds dilute those risks across many holdings.

Systemic risk is market-wide: recessions, liquidity stress, inflation shocks, rate repricing. A three-fund portfolio still carries that risk because retirement growth requires exposure to risk assets.

The advantage is operational discipline. The investor does not need to decide whether health care beats technology, whether Japan beats Europe, or whether small-cap value has finally turned. The portfolio owns the full opportunity set at low cost.

This simplicity also reduces behavioral error. Complex portfolios often create false precision. Ten funds can look diversified while holding the same large U.S. technology names repeatedly. A list of funds is not diversification. Distinct sources of risk are diversification.

The hidden risk: changing the rules too often

The most common failure mode is not choosing VTI instead of a similar U.S. total market ETF. It is changing the plan every time leadership rotates.

A three-fund portfolio will always have a weak sleeve. In some years, international stocks lag. In others, bonds disappoint. During strong U.S. equity cycles, the international and bond allocations may look like dead weight.

That is not evidence the structure is broken. It is evidence that diversification is working as designed. Diversification requires owning assets before they are needed and before they are popular.

A strict investment policy can solve much of this. It does not need to be long. It should state:

- Target allocation by asset class.

- Acceptable drift band, such as 5 percentage points.

- Rebalancing schedule, such as annual review.

- Account placement preferences where relevant.

- Conditions that justify a change, such as retirement date, income shift, or withdrawal need.

“Recent underperformance” should not be on that list.

Implementation: from cash to portfolio

The build sequence should be direct.

First, define the target allocation. Example: 80% stocks, 20% bonds. Then split the stock sleeve between U.S. and international exposure. If the equity split is 70% U.S. and 30% international, the final allocation becomes:

- 56% total U.S. stock market ETF

- 24% total international stock market ETF

- 20% total bond market ETF

That math comes from multiplying the total stock allocation by the regional split:

- 80% stocks × 70% U.S. = 56%

- 80% stocks × 30% international = 24%

Second, select ETFs with broad exposure and low fees. The Vanguard version might use VTI, VXUS, and BND. Equivalent funds can work if they match the same asset-class roles.

Third, decide where purchases occur. In employer retirement plans, the exact ETFs may not be available. Index mutual funds can perform the same function if they cover the same markets at low cost. In IRAs and taxable brokerage accounts, ETFs are usually easier to access.

Fourth, set a contribution rule. New money should reinforce the target allocation. If bonds are underweight, buy bonds. If international stocks are underweight, buy international. This makes rebalancing less intrusive.

Fifth, set a review date. Annual is enough for many investors. Quarterly monitoring can be useful, but frequent checking often increases unnecessary action.

The portfolio should be boring at the transaction level. The capital markets will provide enough movement without extra intervention.

Tax and account placement: keep the claims modest

Tax efficiency depends on account type, income level, fund structure, and local rules. It varies too much to reduce to one universal placement formula.

Still, the general mechanics are clear:

- Tax-advantaged accounts reduce the friction of rebalancing because trades usually do not create current taxable gains.

- Taxable accounts require more care because selling appreciated ETF shares may create capital gains.

- Broad equity index ETFs are often tax-efficient relative to high-turnover active funds.

- Bond income may be taxed differently from qualified dividends, depending on jurisdiction and account type.

This is where precision matters. A three-fund portfolio is simple. Tax treatment is not always simple. The allocation should be designed first; account placement can then be optimized within the investor’s tax constraints.

Do not let tax optimization distort the portfolio’s risk level. A tax-efficient portfolio that is too aggressive near retirement is still too aggressive.

How to evaluate the finished portfolio

The final check is not whether the portfolio looks sophisticated. It should not.

A valid three-fund ETF portfolio for retirement should pass these tests:

1. Each ETF has a distinct role. U.S. stocks, international stocks, and bonds are not overlapping labels for the same risk.

2. The expense ratios are low. Broad index exposure should generally sit near the low-cost range, often around 0.03% to 0.10%.

3. The stock-bond mix matches the time horizon. A long horizon can support more equity risk; a short withdrawal horizon usually requires more stability.

4. The U.S.-international split is intentional. It does not need to be perfect, but it should be stated.

5. The rebalance rule is written. Annual review or a 5% drift band is better than improvisation.

6. The investor understands the drawdown risk. The portfolio can decline during market stress.

7. The strategy avoids performance chasing. Recent winners do not automatically receive higher allocations.

For searchers asking how to check build a three-fund etf portfolio for retirement investing and long-term allocation, this is the essential audit: confirm the asset classes, confirm the cost, confirm the target weights, confirm the rebalance rule.

Everything else is secondary.

Final risk assessment

A three-fund ETF portfolio is one of the cleanest retirement structures available. It provides broad market exposure, low expenses, transparent risk, and a repeatable maintenance process.

The risks are also clear. It will not avoid bear markets. It will not guarantee market-beating returns. It will not solve a poor savings rate, an unstable withdrawal plan, or an allocation that exceeds the investor’s real tolerance for volatility.

The strongest version is built in this order: allocation first, ETFs second, rebalancing third. Reverse that order and the strategy becomes ticker shopping.

For retirement capital, simplicity is not a weakness. It is a control mechanism.